0.7% growth. A record government shutdown. Stagflation risk. This isn’t a soft landing — it’s a warning shot, and real estate operators need to pay attention.

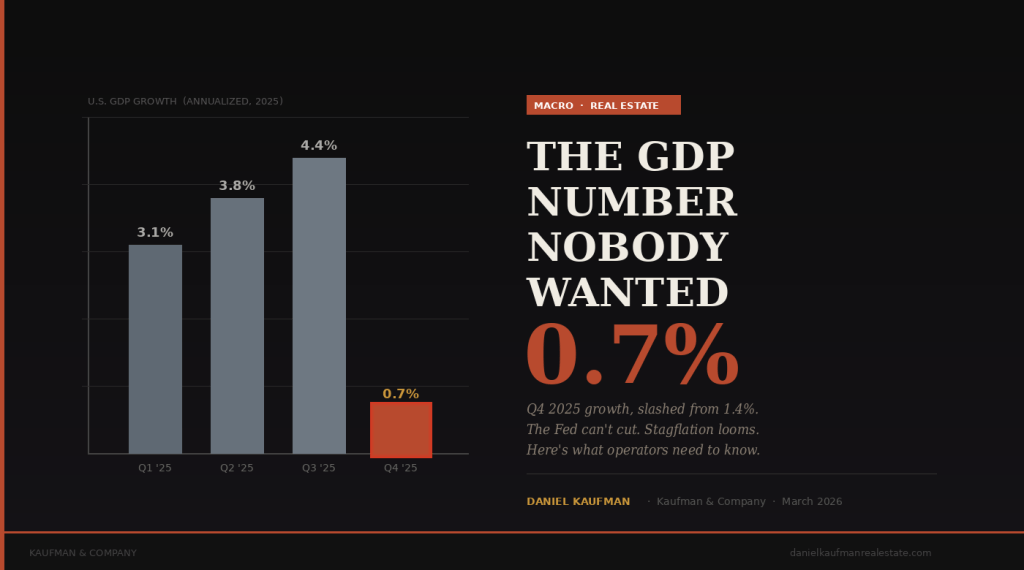

Let’s call it what it is. The second estimate for Q4 2025 GDP just came in at 0.7% annualized growth, half the government’s original read of 1.4%, and a complete gut-punch after 4.4% growth in Q3 and 3.8% in Q2. If you’re in real estate, developing, investing, or just watching the market — you need to understand what that number means and, more importantly, what comes next.

What Actually Happened

The Commerce Department’s revised numbers tell a clear story: the 43-day government shutdown that kicked off October 1st — the longest in U.S. history — shaved more than a full percentage point off Q4 GDP growth on its own. Add a collapse in exports (revised from -0.9% to -3.3%), a pullback in government spending, and cooling consumer activity, and you’ve got an economy that hit a wall heading into year-end. For all of 2025, annual GDP came in at 2.1% — revised down, and the worst full-year performance since the pandemic year of 2020.

For context: we went from 4.4% growth in Q3 to 0.7% in Q4. That’s not a gentle deceleration. That’s a cliff. And it happened in the same quarter that should have been setting up a strong 2026 runway.

Why the Fed Can’t Ride to the Rescue

Here’s where it gets uncomfortable for anyone holding debt or waiting on rate relief. Under normal circumstances, the Fed would respond to a GDP print like this with rate cuts — stimulate the economy, loosen credit, get things moving. That’s the playbook. But this isn’t a normal environment. The ongoing conflict in Iran has sent oil prices surging, with the national average for regular gas hitting $3.63 a gallon — up 9% in a single week. The Fed is not cutting rates into a supply-side inflation shock. It can’t.

As Joel Berner, senior economist at Realtor.com, put it: “This news should lead to rate cuts, but the price pressures in the economy may not allow for them.”

Financial markets have already figured this out.

CME FedWatch puts the probability of the Fed holding rates steady at their current 3.5%–3.75% range at 99.1% at the March 17–18 FOMC meeting. That’s not a coin flip — that’s a near-certainty. Rate relief is not coming this spring. Probably not this summer either, if inflation stays elevated.

The Real Threat: Stagflation

I want to be direct about something too many commentators are dancing around: the risk here isn’t just slow growth or stubborn inflation in isolation. It’s the combination — stagflation. Slow growth plus rising prices. The economy chokes while your costs don’t come down. It’s the policy nightmare because there’s no clean monetary lever to pull.

Cut rates → inflation surges. Raise rates → unemployment spikes and growth collapses. There is no easy exit.

We saw this movie in the 1970s. Oil shocks, Middle East conflict, inflation that wouldn’t quit even as the economy slowed. The Fed under Volcker eventually broke the cycle, but not before years of pain. I’m not saying we’re there yet. I’m saying the preconditions are lining up in a way that deserves serious attention from anyone making capital allocation decisions right now.

What This Means for Real Estate

Let me break this down practically.

On the residential side: the GDP revision itself won’t immediately crater spring home sales, but it will hit consumer confidence — and consumer confidence drives buyer behavior more than any single data point. When people feel uncertain about the economy, they feel uncertain about their jobs. When they feel uncertain about their jobs, they don’t buy houses. Unemployment already ticked up to 4.4% in February, with nonfarm payrolls shrinking by 92,000 jobs. That’s not catastrophic, but the direction matters.

On the commercial and development side: persistent rates in the 3.5%–3.75% Fed funds range means debt costs stay elevated. Cap rates don’t compress. Deals that penciled on the assumption of 2025 rate cuts are going to need to be repriced — or passed on. For operators in the workforce housing and multifamily space, the fundamentals of demand remain intact — people still need affordable places to live — but the financing environment punishes over-leverage and thin margins harder than ever.

The developers who are going to win in this environment are the ones who underwrote conservatively, have patient capital behind them, and aren’t racing to close deals just to put capital to work. Dry powder and discipline are the competitive advantages right now, not aggressive deployment.

My Read

0.7% GDP growth doesn’t mean the economy is in freefall. It means we absorbed a historic self-inflicted wound — a 43-day government shutdown — at exactly the wrong moment. The underlying demand in real estate isn’t gone. Demographics, housing supply shortfalls, and migration patterns haven’t reversed. But the macro environment has shifted from tailwind to headwind, and operators who pretend otherwise are going to get hurt.

Watch the FOMC meeting on March 17–18 closely.

Watch oil prices. Watch the unemployment trend. And if you’re underwriting a deal right now, build in more cushion than you think you need. The market will reward patience over the next 12–18 months.

More soon.

— Daniel Kaufman

Leave a comment