If you’re seeing “one month free,” “six weeks free,” or even “two months free” banners popping up across major Sun Belt cities, you’re not imagining it.

Concessions are back, in a big way.

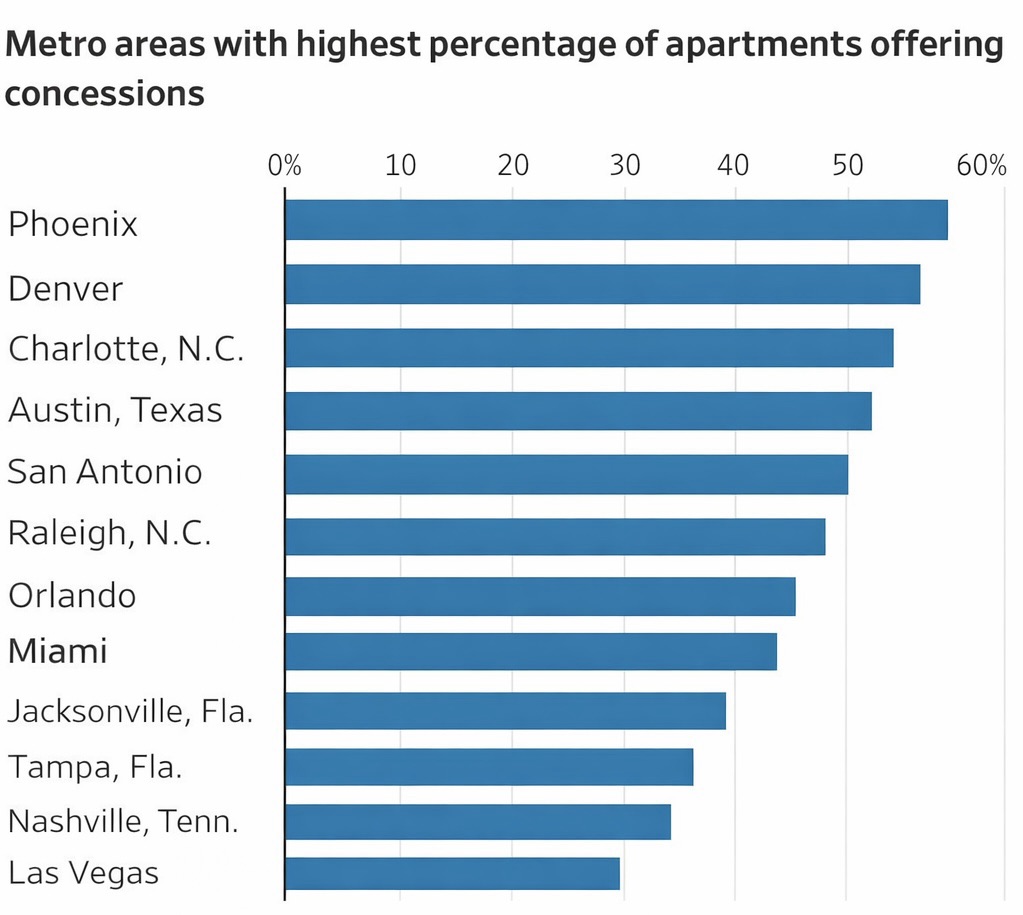

According to recent data highlighted by The Wall Street Journal, more than half of apartment properties in several large U.S. metros are now offering free rent to fill units. Phoenix, Denver, Charlotte, Austin, San Antonio, Raleigh, Orlando, Miami — all north of 40 percent, many north of 50 percent.

That’s not noise.

That’s a market signal.

And it needs to be interpreted correctly.

What the Concession Spike Is Really Telling Us

Concessions are not about generosity. They are about inventory pressure.

The markets topping the chart all share common characteristics:

• Aggressive post-COVID development pipelines

• Heavy Class A concentration

• Rent growth assumptions that ran ahead of fundamentals

• Capital that priced for permanent absorption

Phoenix didn’t suddenly become less desirable.

Austin didn’t stop being a job magnet.

Miami didn’t lose global appeal.

Too much supply arrived at the same time.

When leasing slows, owners don’t cut face rents first. They preserve headline pricing and offer concessions, quietly resetting effective rents lower. That distinction matters far more to investors than the advertised rent number.

Why Chasing “Concession Markets” Is the Wrong 2026 Trade

This is where capital gets misallocated.

Widespread concessions don’t automatically mean opportunity. When half the market is offering free rent, you’re not competing against weak operators. You’re competing against structural oversupply.

And in many of these markets, thousands of additional units are still scheduled to deliver through 2026.

That brings us to the far more important question.

Where Concessions Aren’t Showing Up

The most interesting data isn’t where free rent is everywhere.

It’s where it’s rare.

Markets with limited or no concessions tend to have:

• Real supply constraints

• Zoning, geographic, or political friction

• Slower entitlement timelines

• Less speculative institutional overbuilding

• Durable renter demand

These are the markets that quietly protect downside and preserve pricing power.

The Markets That Actually Make Sense for 2026–2027

Midwest Markets With Supply Discipline

These aren’t boom-and-bust cities. They are stable, demand-driven metros where building is slower and underwriting remains grounded.

Examples:

Chicago (select infill submarkets) Milwaukee Madison, WI Grand Rapids Des Moines

Chicago is a perfect illustration. Despite the headlines, very little new multifamily supply is coming online relative to demand, especially in established neighborhoods. Outside of a handful of ultra-luxury towers, concessions remain limited.

Northeast & New England, Where It’s Simply Hard to Build

These markets rarely lead growth rankings, but they also rarely implode.

Examples:

Boston outer core and suburban nodes Providence Portland, Maine Manchester–Nashua, New Hampshire Select Upstate New York metros

Zoning resistance, land scarcity, environmental regulation, and slow approvals prevent developers from flooding these markets. That friction is precisely what protects rents during down cycles.

Mountain, Resort, and Lifestyle-Constrained Markets

Demand in these markets is structural. Supply is capped.

Examples:

Bozeman, Montana Jackson Hole, Wyoming Park City, Utah Bend, Oregon Truckee / Tahoe submarkets

Vacancy is low not because rents are cheap, but because units don’t sit empty. Concessions are rare, even during broader market slowdowns.

Secondary Southern & Mid-Atlantic Cities That Avoided Overbuilding

Not all Sun Belt cities overdid it.

Examples:

Richmond, Virginia Knoxville, Tennessee Chattanooga, Tennessee Roanoke, Virginia Select submarkets in Huntsville, Alabama

These cities grew steadily, not speculatively. They didn’t attract massive institutional pipelines, and they didn’t assume perpetual rent acceleration. As a result, they didn’t need to “buy” tenants with free rent.

The Common Thread

Every one of these markets shares the same DNA:

• Supply is constrained

• Development is slow, complex, or unpopular

• Rent growth is modest but durable

• Vacancy volatility is low

• Concessions are the exception, not the strategy

That’s not accidental.

That’s structural.

Why This Matters for 2026–2027

The next cycle will not be won by chasing yesterday’s growth markets.

It will be won by:

Building where supply cannot easily follow Investing where rents hold without incentives Prioritizing predictability over hype

The cities topping the concession charts are telling you where the last cycle ended.

The cities with few concessions are quietly telling you where the next cycle will be built.

That’s where capital should be leaning in 2026 and 2027.

And that’s exactly where we’re focused.

Leave a comment