If your clients are shopping for homes this spring, they better come with cash—and plenty of it.

A new report from Realtor.com reveals that down payments have reached their highest Q4 levels on record, continuing a long-term climb that’s reshaping buyer behavior and market dynamics alike.

Whether you’re advising buyers, structuring deals, or eyeing exit strategies on your investment properties, these numbers matter.

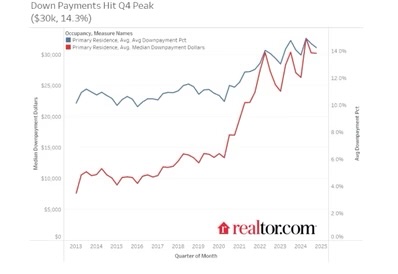

The Data: Bigger Checks, Smaller Pool of Buyers

From October through December 2024, the average down payment hit $30,250, or 14.4% of the purchase price. That’s $1,000 more than the same period a year earlier and marks the highest Q4 average in the report’s history, going back to 2013.

While it’s slightly down from the Q2 2024 all-time peak of 15.1% and $32,700, it reflects a persistent trend: homebuyers are putting more money down than ever before.

Compared to Q4 of 2019—just before the pandemic reshaped the market—down payments are up 3.4 percentage points.

Why Are Down Payments Rising?

Blame it on a combination of high home prices, elevated mortgage rates, and a shifting buyer pool. Today’s active buyers are typically more affluent and less rate-sensitive, which leads to larger down payments.

“This is a market that’s filtering out budget-conscious buyers,” says Daniel Kaufman, founder of Kaufman Real Estate. “Whether you’re a broker, a builder, or an investor, the shift toward high-net-worth activity is changing the playbook—less volume, higher margins, and more competition for move-in-ready product.”

Higher mortgage rates are also incentivizing buyers to put down more up front to reduce their loan size and monthly payments—a rational strategy in a 6–7% interest rate environment.

Investment & Second-Home Buyers: A Slight Retreat

There’s one wrinkle in the data: down payments on second homes and investment properties actually declined slightly in Q4 2024.

• Investment properties: Down to 27.4% of the purchase price (–0.6 percentage points YoY)

• Second homes: Dropped to 28% (–0.8 percentage points YoY)

Even with these modest declines, second-home and investment buyers still wrote checks that were 2.5x larger than the average primary residence buyer.

This group remains strong—but slightly more strategic as high prices, high rates, and increased regulations pressure the economics of non-primary purchases.

First-Time & FHA/VA Buyers: Squeezed Hardest

First-time buyers and those using FHA/VA loans made modest down payments—defined as the 30th percentile in the data set—which climbed 6.5% YoY to $8,200 in Q4 2024.

Compare that to the $4,600 average modest down payment in 2019, and it’s clear how much harder the market has become for new entrants. These buyers face stiff competition, rising costs, and limited inventory.

What’s Next?

Unless mortgage rates fall meaningfully, down payments are likely to stay elevated.

Rates have dipped slightly from January’s 7%+ highs, but remain in the mid-6% range—high enough to deter budget-conscious buyers. Meanwhile, homes priced above $750,000 saw a 7.4% surge in activity, while lower-priced inventory lagged.

In short, the market continues to skew toward buyers with capital, and that’s not likely to change without a drop in rates or a spike in supply.

About Daniel Kaufman & Kaufman Real Estate

Daniel Kaufman Real Estate is a boutique real estate advisory and investment platform led by Daniel Kaufman. With over two decades of experience in brokerage, development, and capital markets, the firm offers strategic insight and hands-on execution across residential, multifamily, and commercial real estate transactions. From market timing to portfolio strategy, Kaufman Real Estate helps clients navigate complex markets with clarity and conviction.

Stay ahead of the market.

Subscribe to the blog for real-time insights, sharp analysis, and what today’s data means for tomorrow’s deals.

Leave a comment